When it comes to life insurance, two of the most common options are term life and whole life insurance. Both can provide financial protection for your loved ones, but they work in very different ways. Understanding the differences can help you choose the policy that best fits your needs and budget.

The biggest differences between term and whole life insurance come down to cost, policy length, and cash value. Term life insurance is more affordable, covers you for a specific period of time, and does not build cash value. Whole life insurance, on the other hand, is more expensive, but it lasts your entire life and includes a savings-like component that grows over time.

What’s the Difference Between Term and Whole Life Insurance?

Term Life Insurance

- Cheaper: Term life is generally the most budget-friendly type of life insurance.

- Temporary: Policies are designed to last for a set number of years, such as 10, 20, or 30.

- No Cash Value: You cannot borrow against or cash out a term policy — it’s pure protection.

Whole Life Insurance

- More Expensive: Whole life usually costs much more than term coverage.

- Permanent: Policies are designed to last your entire lifetime, often up to age 100 or beyond.

- Builds Cash Value: A portion of your premium goes into a cash value account that grows at a guaranteed rate. Over time, you may be able to borrow from it or even surrender the policy for cash.

Term Life vs. Whole Life Insurance: Overview

To see how these two types of coverage stack up, it helps to break down how each one works in practice.

Term Life Insurance

Term life is straightforward. You choose a coverage period — often 10, 20, or 30 years — and if you pass away during that time, your beneficiaries receive the payout. If you outlive the term, the policy ends and no money is paid out. Most people buy level term policies, which means the premiums and death benefit stay the same for the entire term. There are also decreasing term policies, where the benefit shrinks over time, but those are less common. The best way to choose your term length is to think about your biggest financial responsibilities. For example, new parents might select a 20-year policy to ensure their kids are financially protected until adulthood.

Pros of Term Life Insurance

- Affordable Coverage: Term life lets you buy a significant amount of protection at relatively low rates, especially if you’re young and healthy.

- Simple and Straightforward: Term policies focus solely on a death benefit. With a level term policy, both your coverage amount and premium remain the same throughout the term, making it easy to understand and manage.

Cons of Term Life Insurance

- No Lifetime Protection: Once the term ends, your coverage expires. If you still need protection, you’ll have to purchase a new policy, often at higher rates.

- No Cash Value: Term life doesn’t build savings or cash value. Unlike whole life insurance, you can’t borrow against it or access any money while you’re alive — the policy only pays out when you pass away.

Whole Life Insurance

Whole life is the most common type of permanent life insurance. Unlike term, it doesn’t expire after a set number of years. Instead, it lasts your whole lifetime, often until age 100 or 120. Because of this lifelong protection, premiums are much higher compared to term. One of the unique features of whole life insurance is its cash value component. Part of your premium goes into a savings-like account that grows at a fixed, guaranteed rate. This money can be borrowed against or even cashed out, though doing so will reduce your death benefit. Many whole life policies may also pay dividends, which can be used to increase the cash value or reduce premiums.

Pros of Whole Life Insurance

- Lifetime Protection: Whole life insurance covers you for your entire life as long as you keep up with your premium payments. This ensures your beneficiaries will receive a payout no matter when you pass away.

- Cash Value Growth: A portion of your premiums goes into a cash value account, which grows over time. You can use this cash to pay premiums or cover other expenses during your lifetime.

- Dividends: Some policies may pay dividends, which can increase your cash value or reduce your premiums, giving you additional financial flexibility.

Cons of Whole Life Insurance

- Higher Cost: Whole life premiums can be six to ten times higher than term life insurance, making it a significant financial commitment.

- Complexity: Whole life policies are more intricate than term policies. It’s important to carefully read and understand your policy, including how premiums, cash value, and dividends work.

- Cash Value Considerations: If there’s money left in your policy’s cash value account when you pass away, it may not go to your beneficiaries — the insurance company can retain it depending on the policy rules.

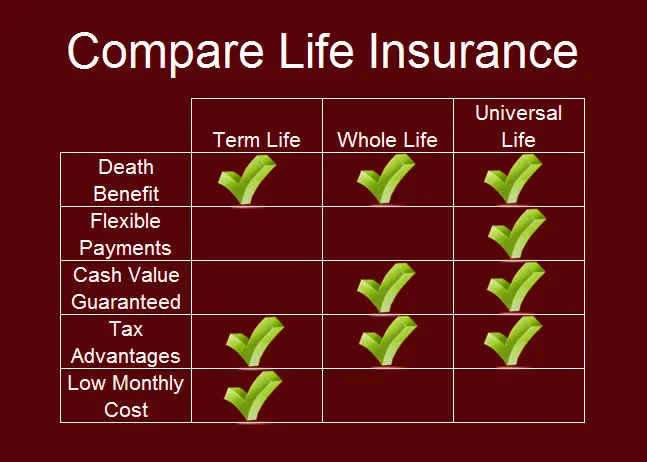

Choosing between term and whole life insurance can feel confusing, but a side-by-side comparison makes it easier to see the differences at a glance.

| Feature | Term Life Insurance | Whole Life Insurance |

|---|---|---|

| Duration | 1–30 years | Your lifetime (or up to 99 years, depending on the policy) |

| Cost | Lower cost | Higher cost |

| Cash Value | No | Yes |

| Medical Exam | Often required | Yes |

| Convertibility | Often available | Sometimes available |

| Loans | Not available | Can borrow against cash value |

Cost of Whole Life Insurance vs. Term Life Insurance

One of the biggest differences between whole life and term life insurance is the cost. Term life is usually the most affordable option because it provides coverage for a limited time and doesn’t include any savings component. Whole life premiums are much higher because the policy lasts your entire lifetime and builds cash value along the way.

To give you a sense of how big the price gap can be, here’s a comparison of average annual premiums for a healthy non-smoker buying $500,000 of coverage. The numbers show how rates increase with age and how much more expensive whole life is compared to term.

| Age & Gender | 20-Year Term Policy | Whole Life Policy |

|---|---|---|

| 20-year-old woman | $177 | $2,695 |

| 20-year-old man | $216 | $3,014 |

| 30-year-old woman | $187 | $3,959 |

| 30-year-old man | $221 | $4,311 |

| 40-year-old woman | $282 | $5,860 |

| 40-year-old man | $334 | $6,387 |

| 50-year-old woman | $642 | $9,037 |

| 50-year-old man | $819 | $10,069 |

| 60-year-old woman | $1,651 | $14,635 |

| 60-year-old man | $2,351 | $16,698 |

| 70-year-old woman | $7,994 | $25,631 |

| 70-year-old man | $9,436 | $29,302 |

As you can see, term life stays relatively affordable through your 30s and 40s, but costs climb with age. Whole life, however, is consistently far more expensive at every age bracket. That’s why many people choose term life when they mainly want affordable coverage during their peak earning years, while whole life is often considered by those looking for permanent protection and long-term cash value growth.

How to Choose Between Term and Whole Life Insurance

For most people, term life insurance is enough to provide the financial protection they need. However, whole life and other permanent policies can make sense in specific situations. The right choice really depends on your goals, budget, and long-term financial plans.

Choose Term Life If You:

- Want the most affordable coverage. Term life is usually the cheapest option, especially if you’re young and healthy.

- Only need coverage for a certain period of time. This could be while you’re raising children, paying off a mortgage, or covering other major financial responsibilities.

- Might want permanent life insurance later but can’t afford it now. Many term policies allow you to convert to permanent coverage later, though the rules and deadlines vary.

- Don’t care about building cash value. With term, you’re paying purely for protection, which leaves you free to invest the money you save compared to whole life premiums.

Choose Whole Life If You:

- Can comfortably afford higher premiums. Whole life is a long-term commitment, and missing payments could cause your policy to lapse.

- Want lifetime protection. Whole life policies pay a death benefit whenever you pass away, as long as the policy stays active. This ensures your beneficiaries will receive a payout no matter when you die.

- Have a lifelong dependent. For example, parents of a child with disabilities often use life insurance to fund a trust that provides care after they’re gone. This requires careful planning with a financial advisor or attorney.

- Want guaranteed cash value growth. Whole life policies grow cash value at a fixed rate, which can be borrowed against or used in other ways while you’re still alive.

How to Get Life Insurance

Applying for life insurance and getting approved can take a few weeks, but knowing the steps ahead of time makes the process much easier.

1. Decide on the type of policy. Before you apply, think about whether term life, whole life, or another type of policy fits your goals and budget. Understanding the differences will help you choose coverage that meets your needs.

2. Determine how much coverage you need. The right amount depends on factors like your income, number of dependents, living expenses, debt, and any future costs you want your policy to cover, such as college tuition or a mortgage.

3. Compare quotes. Shopping around can help you find the best rate. You can get quotes online or work with a broker who can compare multiple insurers and explain the differences in features and pricing.

4. Submit your application. You’ll need to provide details about your lifestyle and health, including your age, gender, weight, medical history, family health history, occupation, and more.

5. Complete a medical exam (if required). Many policies require a medical exam to assess your risk. The insurer may send a practitioner to your home or ask you to visit a clinic.

6. Purchase your policy. Once approved, you’ll receive your final rate and can choose to accept or decline. Your policy becomes active once you make the initial payment. Make sure you understand any waiting periods or conditions that could affect the payout to your beneficiaries, as well as factors that might cause the policy to lapse.

Getting life insurance may seem complicated at first, but following these steps helps ensure you get the coverage you need for yourself and your loved ones.

Alternatives to Term and Whole Life Insurance

If you like the idea of permanent coverage but want more flexibility than traditional whole life offers, there are other types of policies worth considering. These include:

- Universal life insurance

- Variable life insurance

- Variable universal life insurance

- Indexed universal life insurance

Each of these has different cost structures, investment options, and potential risks. Some give you the chance to grow cash value based on market performance, but that can also mean higher expenses or uncertainty.

Because life insurance is such a long-term financial decision, it’s always smart to talk with a fee-only life insurance consultant or financial advisor who can help you weigh the pros and cons for your specific situation.

Frequently Asked Questions About Term and Whole Life Insurance

What happens to term life insurance at the end of the term?

Term life insurance is temporary, so once your policy term ends, your coverage expires. If you still want protection, you’ll need to buy a new policy — usually at higher rates since you’ll be older. Some term policies also allow you to convert to permanent life insurance before a set deadline, which lets you keep coverage without reapplying for health approval.

Why is term life insurance cheaper than whole life?

Term life is more affordable because it’s straightforward coverage. It only lasts for a set number of years and doesn’t include a savings feature. Whole life, on the other hand, provides lifetime protection and builds cash value, which makes it much more expensive.

Does term life insurance build cash value?

No, term life insurance doesn’t have a cash value. It’s designed purely for protection. If building value over time is important to you, a permanent policy like whole life or universal life may be a better fit.

Which is better: whole or term life insurance?

For most people, term life insurance provides enough coverage at the lowest cost. It’s a smart choice if your main goal is to protect your family during your working years. Whole life might be worth exploring if you have lifelong dependents, want guaranteed cash value growth, or are already maxing out other savings and retirement options.

What are the main differences between term and whole life insurance?

The key differences come down to cost, length, and cash value. Term life is affordable but temporary, covering you for 10, 20, or 30 years. Whole life is much more expensive but lasts your entire lifetime and includes a cash value component that grows over time.

")